What is a Medicare Supplement or Medigap Insurance?

Medicare supplement insurance (Medigap) helps pay some of the out-of-pocket health care costs that Original Medicare (Parts A and B) doesn’t pay. It isn’t a government benefit, like Parts A and B. Plans are offered through private insurance companies. It’s your decision whether to add a supplement with your Original Medicare.

There are 10 standardized Medicare supplement insurance plans, labeled “A” through “N.” (These letters are not related to the Medicare Part A, B, C and D) The main purpose of a Medicare supplement plan is to cover some of the out-of-pocket costs not paid by Medicare Parts A and B. This includes deductibles, co-pays and co-insurance. Each of the standardized plans provides benefits for different out-of-pocket costs.

The most popular plans with my clients are Plan N and Plan G.

Each standardized plan with the same letter must offer the same basic benefits, no matter which insurance company is offering the plan. For example, the basic benefits of one company’s Plan G are the same as the basic benefits of another company’s Plan G. However, the premium cost of a plan could be different between insurance companies in a service area; and many states and zip codes are rated at different premiums for the same plan.

Medigap plans do not include prescription drug, so you need to add a stand alone drug plan if you would like Part D coverage. Medigap plans are secondary to Original Medicare, so you can go to any provider or facility in the United States that accepts Medicare. Most Medigap plans also offer an amount for emergency foreign travel.

You cannot have both a Medigap plan and a Medicare Advantage plan at the same time.

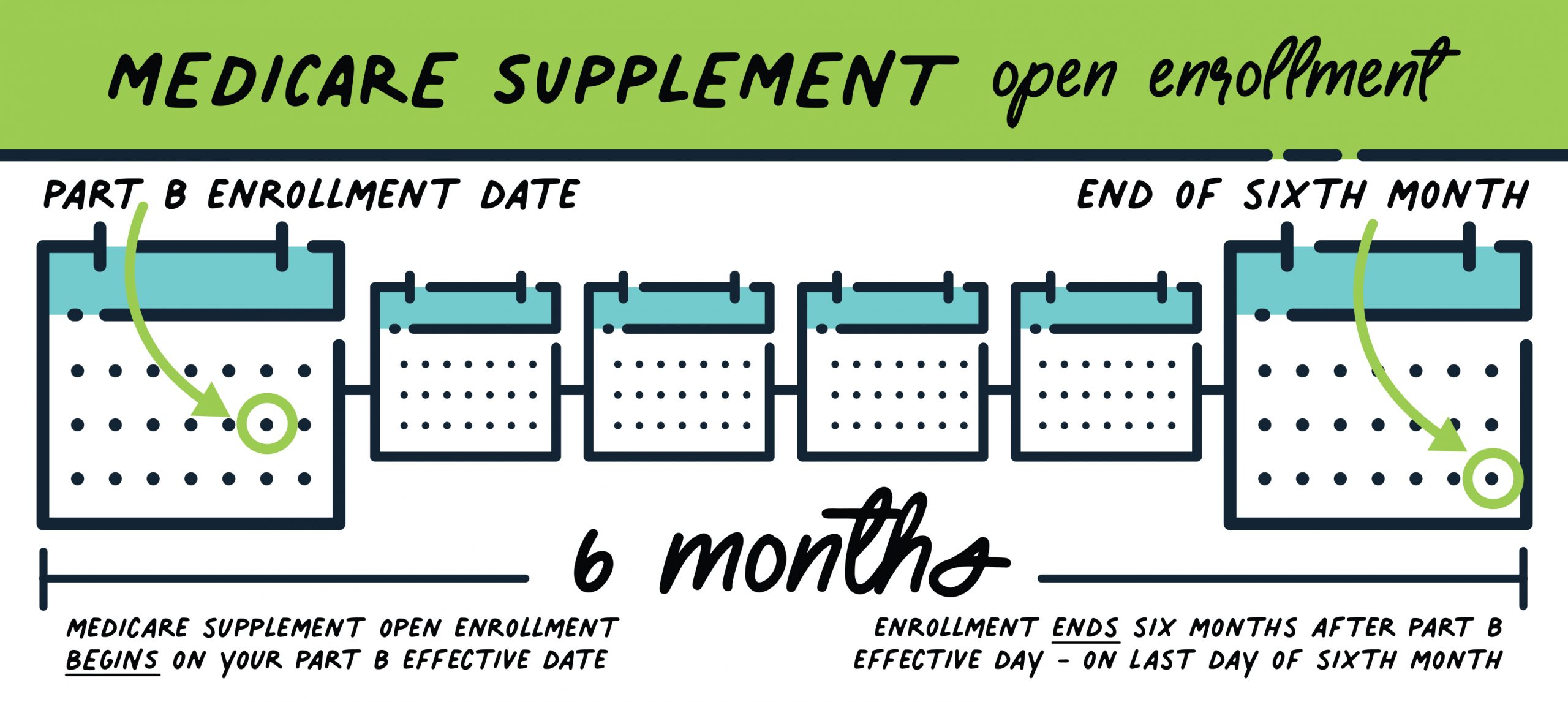

Enrollment for Medigap Policies

When you are new to Medicare Part B, you have a one time six month open enrollment period from your Part B start date where the Medigap companies must accept your application without restrictions, like asking health questions. Sometimes this gets confused with the annual open enrollment period in the fall, but these are not the same thing. Once this Medigap Open Enrollment period ends, you must answer health question (in most cases) to apply for a Medigap policy. Since it is not required for the Medigap policies to accept you unless you have a guaranteed issue right (also called Medigap protections) they can accept or decline you based on the underwriting questions if you are outside of your Open Enrollment Period. Those individuals on Medicare before age 65 will get a second Open Enrollment Period when they turn 65.